Money Roadmap

The Financial Order of Operations: A Money Roadmap That Ends in Your Estate Plan

The step-by-step order to use your money — emergency fund, 401(k) match, debt, IRA, HSA, investing — and the final step almost everyone forgets: your estate plan.

The financial order of operations is a priority-ranked sequence for every dollar you earn: build a starter emergency fund, capture your full employer 401(k) match, pay off high-interest debt, fund tax-advantaged accounts (IRA, HSA), save 15% for retirement, then invest in a taxable account — and finally, plan how it all transfers through your estate. Follow it top to bottom and you never have to guess what comes next.

If you have ever stared at a paycheck and wondered “what should I actually do with this money?”, you are not alone — it is one of the most-asked questions in personal finance. The good news: there is a widely agreed-upon answer, and it is an ordered list, not a guessing game.

This roadmap — often called the financial order of operations — ranks every dollar by the guaranteed return it earns. Follow it top to bottom, skip the steps that do not apply to you, and you will never have to wonder what comes next. And because Sunset connects your money to your estate plan, we have added the one step most guides leave out: deciding where your wealth goes when you are gone.

Why order matters: every dollar has a “best” job

A dollar can only be in one place at a time, so the question is always which job earns the most. The order below is built on a simple idea — chase guaranteed returns first, uncertain returns last:

Paying off a 22% credit card is mathematically identical to earning a guaranteed, tax-free 22% — something no investment can promise. That is why debt payoff outranks investing, and why a free employer match outranks everything.

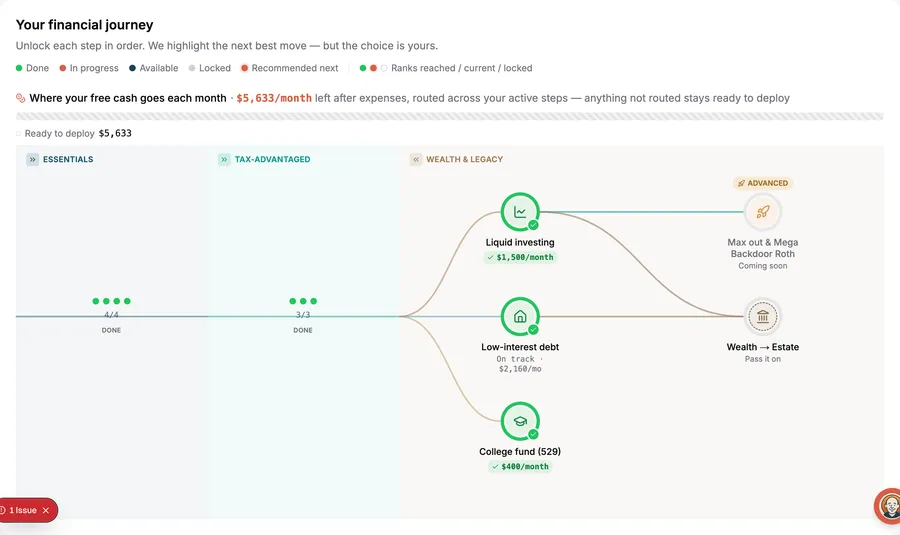

The financial order of operations, step by step

Here is the full sequence. In Sunset’s Money Roadmap, these become a guided, leveled journey that knows what you have already done and highlights your single best next move.

Step 1 — Build a starter emergency fund

Before anything else, set aside a small buffer — about $1,000, or one month of expenses — so a flat tire or medical bill does not go on a credit card. This is a placeholder; you will grow it later in Step 4.

Step 2 — Capture your full employer match

If your employer matches 401(k) contributions, contributing at least enough to get every dollar of the match captures the highest guaranteed return in this list. A “50% match on the first 6%” means contributing 6% adds an instant 50% to what you set aside — which is why it’s rarely worth passing up. (See how the match works →)

Step 3 — Pay off high-interest debt

Attack debt above roughly 8% APR (credit cards, payday loans, many personal loans). Two proven methods:

| Method | How it works | Best for |

|---|---|---|

| Avalanche | Pay extra on the highest interest rate first | Paying the least total interest (mathematically optimal) |

| Snowball | Pay off the smallest balance first | Motivation and quick wins |

Both work — the best method is the one you will stick with.

Step 4 — Finish your emergency fund (3–6 months)

Now grow the buffer from Step 1 into a full 3–6 months of expenses (9–12 months if your income is variable), held in a safe, liquid place like a high-yield savings account. (How much do you actually need? →)

Step 5 — Fund an IRA and an HSA

These tax-advantaged accounts are your next priority:

An HSA (if you have a qualifying high-deductible health plan) is uniquely powerful — it is the only account that is tax-free going in, growing, and coming out for medical costs. The IRA decision between Roth and Traditional comes down to your tax bracket now versus in retirement. (Roth vs. Traditional, and what it means for your heirs →)

Step 6 — Save 15% of your income for retirement

Round out your retirement savings — going back to your 401(k) after maxing the match — until you are saving about 15% of gross income (including the match). Behind on savings? Aim for 20%.

The 15% rule of thumb

Counting your employer match toward the 15% is fine. If 15% feels impossible today, start at 10% and raise your contribution by 1% every year — most people never feel it.

Step 7 — Invest in a taxable account and save for other goals

Once retirement is on track, use a regular brokerage account for additional investing, and tackle goals like a 529 college fund, a home down payment, or paying off low-interest debt early. There is no penalty and no contribution limit here — it is your flexible money.

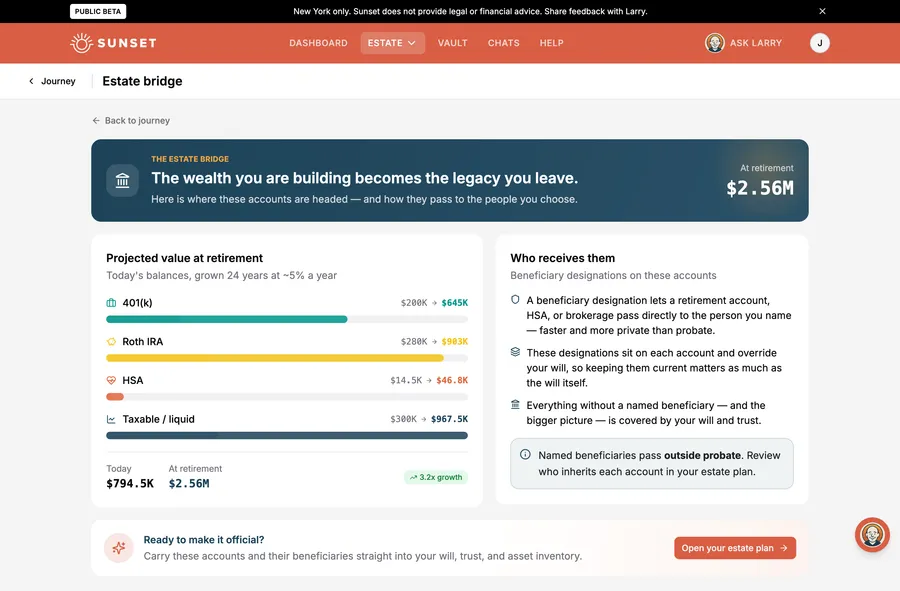

Step 8 — Plan where it all goes: your estate

This is the step the other guides forget. Every account you just built needs a transfer plan. Without one, the wealth you spent decades growing can get stuck in probate, go to the wrong person, or hand your heirs an avoidable tax bill.

Your money and your will don't control the same assets

Retirement accounts, HSAs, life insurance, and “transfer-on-death” brokerage accounts pass to whomever you named as beneficiary — and that designation overrides your will. Everything else flows through your will. Getting these two in sync is the real finish line of the roadmap. See exactly which asset goes where →

Where most people go wrong

- Skipping the match to pay off low-interest debt. A 4% car loan should never come before a 50% match.

- Investing in a brokerage before maxing tax-advantaged accounts. You are leaving tax savings on the table.

- Never naming or updating beneficiaries. An outdated 401(k) form naming an ex-spouse generally overrides your brand-new will. (Why beneficiary designations win →)

- Treating the estate step as “later.” The accounts grow whether or not you plan for them — the plan should grow too.

From roadmap to legacy

The financial order of operations works because it removes guesswork: do the steps in order, and your money is always doing its highest-value job. The last step — your estate plan — is what turns a lifetime of disciplined saving into a legacy that actually reaches the people you love.

Sunset is the only place that does both. The Money Roadmap guides you through every step above, and its final stop — the Estate Bridge — carries your accounts and beneficiaries straight into your will and trust.