Money Roadmap

Employer 401(k) Match: Why It Is Free Money and How to Capture All of It

Capture your employer 401(k) match — a guaranteed instant return up to 100%. Learn the vesting rules, true-up mechanics, and how to avoid the front-loading trap.

An employer 401(k) match is about the closest thing to free money in personal finance. If you contribute 6% of your salary and your employer offers a 50% match on that amount, the match instantly adds 50% to what you set aside — no market timing or luck required. (Two caveats worth knowing up front: a vesting schedule may apply before the match is fully yours, and once the money is invested it rises and falls with the market like any other balance.) Yet millions of US workers leave the match uncaptured every year — by contributing too little, front-loading early in the year, or misunderstanding when the money actually belongs to them.

This is the second step in the Money Roadmap — after an emergency fund and before high-interest debt payoff — because no other financial move offers a guaranteed, immediate return.

How the employer match works: the math

Your employer does not automatically contribute to your 401(k). Instead, they match a percentage of what you contribute. The most common match formula is 100% on the first 3% of your salary, plus 50% on the next 2%.

Here’s what that looks like in practice:

| Your contribution | Employer match | Total that year |

|---|---|---|

| 3% of salary | 3% (100% match) | 6% |

| 4% of salary | 3.5% (100% on first 3%, 50% on the next 1%) | 7.5% |

| 5% of salary | 4% (100% on first 3%, 50% on the next 2%) | 9% |

| 6% or more | 4% (match caps after 5% contribution) | 10% or more |

To capture the full match, you need to contribute at least 5% of your gross pay. If you contribute less, you leave money on the table.

Let’s work through a concrete example. You earn $60,000 per year and contribute 5% ($3,000 per year, or roughly $115 per paycheck). Your employer contributes 4% ($2,400 per year). You have just earned a $2,400 return on a $3,000 contribution — an 80% instant return — before the money is invested in the stock market.

The math is so powerful that financial advisors often say your employer match should be your first retirement move after you have a small emergency fund and before you pay off low-interest debt.

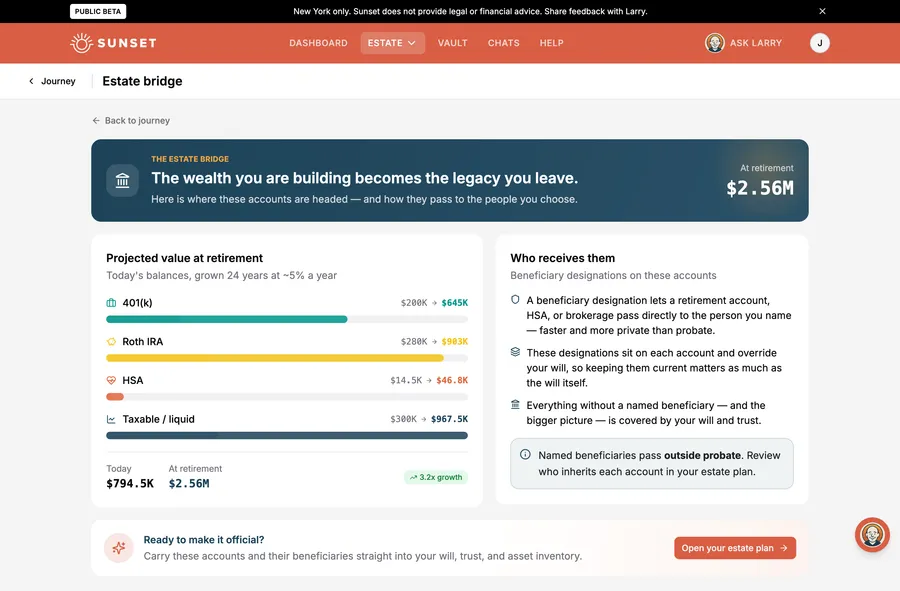

Your 401(k) match is controlled by a beneficiary designation, not your will

When you die, your 401(k) and all its accumulated match go to whoever you named on your plan’s beneficiary form. That designation overrides your will, probate, and state law. If you never named anyone—or named an ex-spouse—the money goes there, not to your spouse or children. Update this form every time your life changes. Learn which assets actually go to your heirs, and why beneficiary designations matter so much.

Vesting: when the match truly belongs to you

Contributing to your 401(k) makes your contributions immediately and permanently yours. But your employer’s match is different. Employers use a vesting schedule to phase in ownership of their contributions over time, as an incentive for you to stay with the company.

There are three common vesting schedules:

-

Cliff vesting — You own 0% of the employer match until a set date (usually 3 years), then you own 100%. If you leave one day before the cliff date, you forfeit all of it.

-

Graded vesting — You gain ownership in steps. For example, 20% after 2 years, 60% after 4 years, 100% after 6 years. If you leave after 3 years, you keep 40% of the match.

-

Immediate vesting — You own the match as soon as your employer makes it. Many plans vest immediately (safe-harbor matches are required to), while others use a cliff or graded schedule—so check which one yours uses.

Check your plan documents or ask your benefits manager which type you have. If you are planning to leave a job, knowing your vesting schedule can mean the difference between walking away with the full match or losing thousands.

The front-loading trap: how to avoid losing match all year

Here’s a subtle and costly mistake that high earners often make: they contribute aggressively to their 401(k) in the first few months of the year, hit the $24,500 annual limit (2026) by April or May, and then stop contributing. Once they stop, the employer also stops matching—for the rest of the year.

Why? Most employers calculate the match on a per-paycheck basis. If you do not contribute from a paycheck, your employer does not contribute, either. So if you max out early and quit contributing, you miss months of match dollars.

Here’s the gap in dollars. Suppose you earn $240,000 per year (paid 24 times per year) and your employer matches 50% of the first 6% of salary. If you contribute evenly across all 24 paychecks at 10.2%, you earn a $7,200 match. But if you front-load and hit the limit by June, you earn only a $3,600 match — you left $3,600 on the table.

Check whether your plan offers a true-up

Many employers offer a “true-up” contribution at year-end to restore the match you would have earned if you had spread your contributions evenly. But not all do. If your plan does not and you front-load, you will miss match dollars for the rest of the year. Ask your HR or benefits team: “Does our plan offer a year-end true-up?” If the answer is no, spread your contributions across all paychecks instead of front-loading.

How much should you contribute?

A common baseline is to contribute at least enough to capture the full match—for many plans, that is around 5% of gross salary. If cash flow is tight, some people start there and raise it by 1% a year.

If you can afford more, the Money Roadmap suggests working up to 15% of gross pay across all retirement savings (employer match plus your own contributions). Many financial advisors use this as a rule of thumb: if 15% feels impossible, you are likely not saving enough elsewhere, or you have high-interest debt to pay down first.

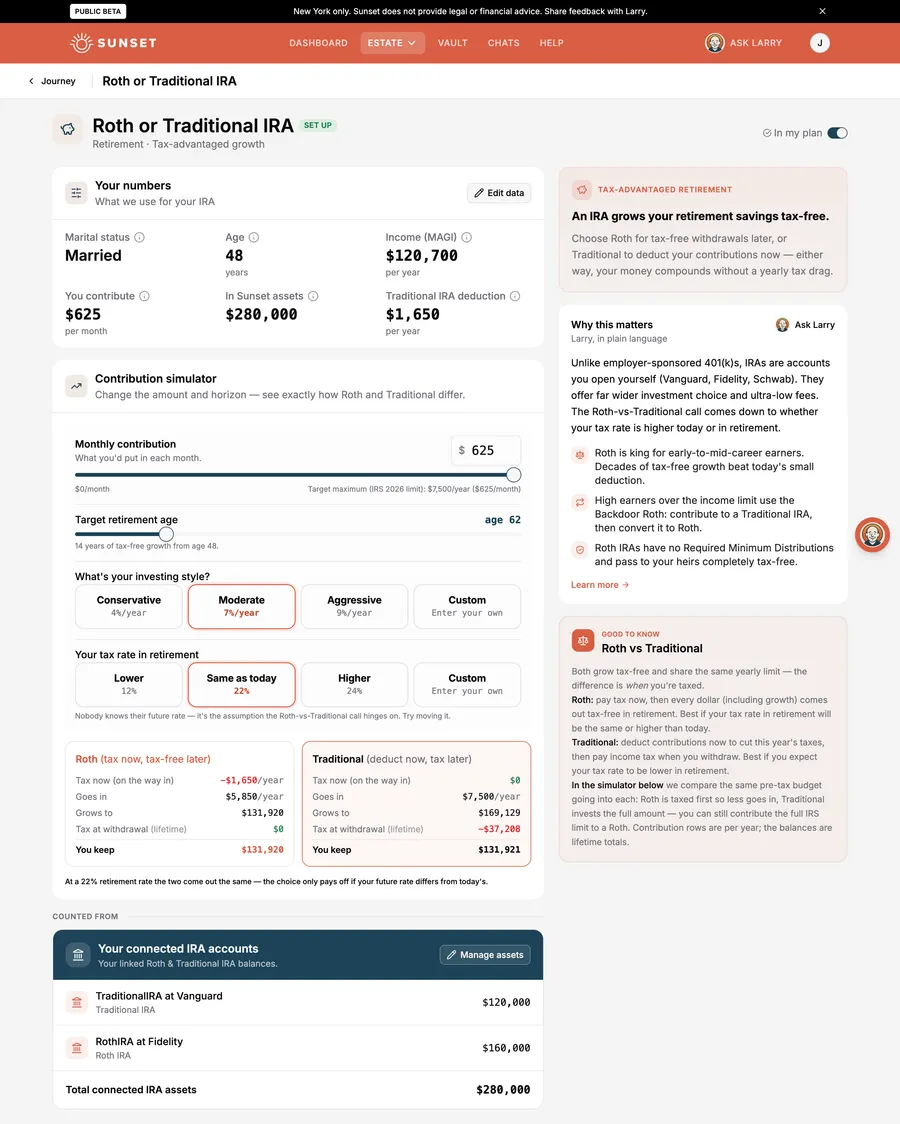

If your prior-year FICA wages (shown on your Form W-2, Box 3) exceeded $150,000, be aware of a SECURE 2.0 rule that requires higher earners’ catch-up contributions to be made as Roth (after-tax) rather than pre-tax. The statutory requirement took effect January 1, 2026, but the IRS is treating 2026 as a transition year—plans may apply a reasonable good-faith interpretation, and the final regulations generally apply to contributions in tax years beginning after December 31, 2026. So if you are 50 or older and a high earner, check whether your plan is already requiring Roth catch-ups. Your employer’s match is unaffected either way.

Use the max to your advantage — after you capture the match

Once you have captured the full employer match, additional contributions come straight from your paycheck and do not earn that instant boost. The long-term growth of a 401(k) is still valuable. A widely used order of operations is the match first, then high-interest debt, then additional retirement savings—the Money Roadmap walks through it, but your own rates and goals determine what fits.

What happens to your match when you change jobs

If you leave your employer and you are fully vested, your match stays in the 401(k). You can roll it into an IRA or your new employer’s plan. If you are not fully vested (e.g., you leave before the three-year cliff vesting date), you forfeit the unvested portion—it goes back to your employer.

This is one reason to know your vesting schedule before you resign. If you are close to the vesting date, waiting a few weeks or months might be worth thousands of dollars.

From match to legacy: connecting your 401(k) to your estate plan

The money in your 401(k)—including every dollar of employer match—grows tax-deferred over your working years. When you retire, you start withdrawals. When you die, it passes to your beneficiary.

This is step 2 of the Money Roadmap. Step 1 is your emergency fund. Step 3 is paying off high-interest debt. Together, they form the foundation of a plan that ends in a well-structured will and beneficiary designations.

Your 401(k) and its beneficiary designation are two of the most powerful wealth-transfer tools you own. Unlike your will, which goes through probate and can be challenged, your beneficiary designation is private and immediate. The money flows straight to the person you named, bypassing probate entirely.

Learn exactly where every type of account goes when you die — and which beneficiary designations override your will. Then use the Money Roadmap to make sure you are capturing every guaranteed return along the way.

Sources

- 1.401(k) Limit Increases to $24,500 for 2026, IRA Limit Increases to $7,500(irs.gov)

- 2.Retirement Topics - 401(k) and Profit-Sharing Plan Contribution Limits(irs.gov)

- 3.How Does a 401(k) Match Work? | Average 401(k) Match | Fidelity(fidelity.com)

- 4.Issue Snapshot - Vesting Schedules for Matching Contributions | IRS(irs.gov)

- 5.401(k) Front-Loading: Is It a Smart Move or a Cash-Flow Trap?(henssler.com)

- 6.401(k) True-Up: Avoid Missing Your Employer Match(equityftw.com)

- 7.2026 Amounts Relating to Retirement Plans and IRAs(irs.gov)

- 8.Different 401(k) Employer Match Types (With Examples) | Human Interest(humaninterest.com)