Wealth & Will

Where Your Money Goes When You Die: A Map of Every Account From Emergency Fund to 529

Learn where each account—401(k), IRA, brokerage, 529, HSA, life insurance—goes after death. Probate vs. beneficiary rules and tax treatment for 2026.

When you die, your money does not automatically flow to your heirs through your will. Instead, different accounts follow completely different legal paths, some skipping probate entirely, others moving through it, and still others triggering immediate tax bills. Understanding this map is the difference between a clean inheritance and a delayed, costly mess—and it is exactly the bridge between your money roadmap and your estate plan.

The four paths your money can take

Your assets move through one of four legal channels after you die. The channel depends entirely on how the account is titled and whether you named a beneficiary.

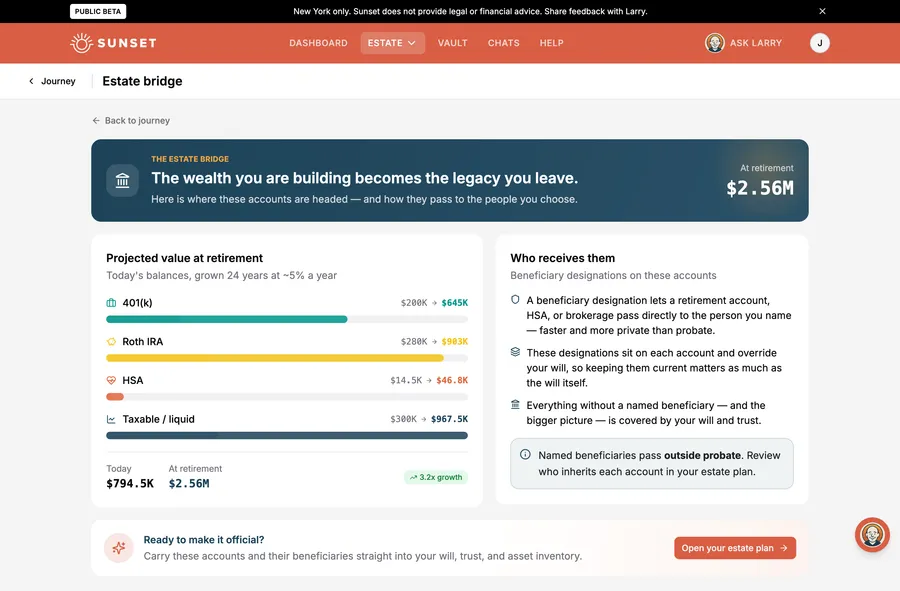

Beneficiary designation (fastest). Retirement accounts (401(k)s, 403(b)s, IRAs), life insurance policies, and accounts marked with a payable-on-death (POD) or transfer-on-death (TOD) designation bypass probate and pass directly to the named beneficiary. The financial institution pays them within weeks. Your will has no say.

Probate (slowest). Assets titled solely in your name with no beneficiary go through probate court. The court oversees inventory, pays creditors, and distributes the remainder to heirs, typically taking 6 months to 2 years.

Joint ownership with right of survivorship. If an account is held jointly with someone else and titled with survivorship rights, it passes automatically to the surviving owner outside probate.

Trust ownership. Assets held in a revocable trust pass to beneficiaries named in the trust, bypassing probate and avoiding public court proceedings.

Most people end up using a mix of these four methods without realizing it. The problem: your will has no authority over beneficiary designations, POD accounts, or jointly owned assets. If your beneficiary designation and your will contradict each other, the beneficiary designation wins.

What happens to each account type

| Account Type | Transfer Path | Tax Treatment | Probate? |

|---|---|---|---|

| 401(k) / 403(b) / 457 plan | Named beneficiary | Income tax on withdrawals (non-spouse); SECURE Act 10-year rule | No |

| Traditional IRA | Named beneficiary | Income tax on withdrawals (non-spouse); SECURE Act 10-year rule | No |

| Roth IRA | Named beneficiary | Tax-free withdrawals (non-spouse); SECURE Act 10-year rule | No |

| HSA | Named beneficiary | Tax-free to spouse (continues as HSA); taxable to non-spouse as ordinary income | No |

| Life insurance | Named beneficiary | Income-tax-free to the beneficiary; but included in your taxable estate if you owned the policy (incidents of ownership) or it’s payable to your estate | No |

| Regular brokerage | Will or probate (if no TOD) | Step-up in basis (fair market value at death); long-term capital gains rates | Yes, unless TOD |

| Savings/checking account | Will or probate (if no POD) | No tax (not income) | Yes, unless POD |

| 529 plan | Successor owner (if named) or probate | No tax if beneficiary unchanged; taxable distribution only if changed to a non-family member; if you superfunded (5-year election) and die within the 5-year period, the post-death portion is added back to your taxable estate | No, if successor named |

| Real estate | Will or probate (if no TOD deed) | Step-up in basis | Yes, unless TOD deed |

| Investment real estate | Will or probate | Step-up in basis (potential depreciation recapture for rental property) | Yes, unless TOD deed |

Retirement accounts: the SECURE Act 10-year rule and beneficiary designations

Your 401(k) and IRA are controlled by the beneficiary designation form you file with your employer or financial institution, not by your will. If you never named a beneficiary, the account follows the plan’s or custodian’s default terms—an ERISA 401(k) usually pays a surviving spouse first, while an IRA with no beneficiary typically passes through your estate and into probate.

If you named someone as beneficiary, they inherit the account outside probate—but they face a strict tax deadline.

Most heirs must empty inherited retirement accounts within 10 years

If you died after January 1, 2020, and your beneficiary is not your spouse or one of a small group of “eligible designated beneficiaries” (your minor child, someone not more than 10 years younger than you, or someone disabled or chronically ill), they must withdraw and pay income tax on the entire account by December 31 of the 10th year following your death. Penalties apply for missing the deadline.

A non-spouse beneficiary who inherits a $500,000 traditional IRA, for example, can spread withdrawals over the 10 years, but must empty it by year 10 and pay ordinary income tax on each dollar withdrawn. (If the original owner had already started required minimum distributions, the beneficiary must also take an annual withdrawal in years 1–9.) An inherited Roth IRA is gentler on taxes: withdrawals are generally tax-free to the beneficiary, even though the 10-year rule still applies.

A surviving spouse has an advantage other beneficiaries don’t: they can roll your IRA into their own or treat it as their own, avoiding the 10-year rule and letting the account keep growing tax-deferred. That flexibility is why many married people name a spouse as primary beneficiary on retirement accounts—though the best choice depends on your family, tax situation, and goals.

Life insurance: the beneficiary form is law

Life insurance death benefits pass directly to your named beneficiary, outside probate and outside your will. The beneficiary form filed with the insurance company on the day you die controls who gets the money—not your will, not your estate, not anything else.

If you never name a beneficiary, or if every named beneficiary has already died, the death benefit goes to your estate and enters probate. This is usually a mistake because it exposes the money to creditor claims and drags out payment for years.

Large life insurance payouts can also trigger federal estate tax if your estate is very large. For 2026, the federal estate tax exemption is $15,000,000 per person, so estate tax on life insurance is rare. New York state tax is much tighter: the basic exclusion is $7,350,000, and New York does not allow portability between spouses, meaning each person loses their unused exemption when they die.

New York's estate tax cliff: a dangerous edge

An estate at or below the $7.35 million exemption owes no New York estate tax. Between there and about $7.72 million (105% of the exemption), the exemption phases out—so an estate of $7.4 million already owes some tax, and a modest overage can trigger a steep bill. Once the estate tops about $7.72 million, the exemption is lost entirely and the full value is taxed at 3.06% to 16%. This cliff makes careful planning important for New York residents with estates in this range.

Brokerage and savings accounts: probate or transfer-on-death

Cash and investments held in a regular brokerage or bank account in your name only will go through probate unless you set up a payable-on-death (POD) or transfer-on-death (TOD) designation.

POD and TOD are free, simple ways to name a beneficiary for bank and brokerage accounts. Unlike retirement accounts, they receive no special tax treatment—but they do skip probate. After you die, the money moves directly to the named beneficiary without court involvement, usually within a few weeks.

The trade-off: POD and TOD designations override your will. If your will says to split your brokerage account equally among three children, but the TOD says it all goes to one child, that child gets it all. This is why you must review all your account titles and beneficiary designations together, not separately.

Inherited brokerage accounts get a huge tax gift: the step-up in basis. If you bought a stock for $50,000 and it is worth $500,000 when you die, your heirs inherit it with a cost basis of $500,000. If they sell it immediately, they owe zero capital gains tax. They only pay tax on gains that happen after the inheritance. This step-up is one of the most powerful estate-planning advantages in tax law and applies to all taxable investments, real estate, and most other assets—but not to retirement accounts.

529 plans: successor owner, not beneficiary

A 529 education savings account is unique because it is not controlled by a beneficiary designation. Instead, you name a successor owner (or account owner) to take over the account if you die.

If you do not name a successor owner, the account typically goes through probate and may become tangled in your estate. Naming a successor owner is a one-time action that avoids this entirely and lets the account stay invested for the child’s education without court delay.

When the successor owner takes over, they can keep the current beneficiary (the child) on the plan, change the beneficiary to another family member (such as a younger sibling), or roll the money to a 529 plan in another state. For the full mechanics, see our guide to 529 plans and estate planning.

A 529 is a completed gift you still control

Money you put into a 529 is generally treated as a completed gift, so it sits outside your taxable estate—yet you keep control of the investments and distributions. One timing exception: if you superfund with the 5-year election and die within that window, the post-death portion is added back to your estate. Naming a successor owner is a separate step—it decides who controls the account and helps it avoid probate. This is general information, not tax advice.

HSAs: the inheritance tax trap

A health savings account (HSA) is a secret estate-planning tool for those who have one, but it contains a dangerous trap for non-spouse beneficiaries.

If you name your spouse as beneficiary, they can inherit the HSA and treat it as their own, continuing to use it tax-free for qualified medical expenses. But if you name anyone else—a child, sibling, or other relative—the account stops being an HSA and its full value becomes taxable income to that beneficiary in the year you die, at their ordinary income tax rate. There is no step-up in basis and no special tax treatment.

A beneficiary who inherits a $100,000 HSA could owe $22,000 to $37,000 in federal income tax alone, depending on their tax bracket, plus state income tax.

There is one narrow escape: a non-spouse beneficiary can use inherited HSA funds to pay the deceased’s medical bills without owing tax, as long as they pay those bills within 12 months of death. This strategy can offset some of the tax bill but rarely eliminates it.

Emergency fund, checking, and savings accounts

Money in a checking or savings account passes to whoever is named on your will or beneficiary designation, whichever exists. If you have a POD designation on a savings account, that beneficiary receives the full balance immediately after your death. If not, it goes through probate.

These accounts receive no step-up in basis (because they are cash, not investments), but they also incur no capital gains tax when inherited.

Emergency funds, checking, and savings accounts should be titled to allow quick access to cash for heirs, burial costs, and immediate expenses. A POD designation is the simplest option. Some people also name a spouse or adult child as a joint owner with survivorship rights, which gives them immediate access while you are alive and passes the account automatically at death.

Bringing it all together: your money roadmap to your will

This map is the bridge between your Money Roadmap and your estate. Your financial order of operations tells you how to build wealth year by year. But the moment you die, the structure of each account—and who you named as a beneficiary—takes over from your will.

If you’ve built wealth in a 401(k), a named beneficiary is what routes it to the person you choose. A brokerage account can use a TOD registration; a 529 can name a successor owner; an HSA left to a spouse keeps its tax-free treatment. These aren’t separate estate-planning tasks—they’re the final step of your money roadmap.

Review your beneficiary designations every two to three years, especially after major life changes like marriage, divorce, or the birth of a child. Your beneficiary form is the one document that overrides your will, so it must reflect your actual wishes.

Start with the Money Roadmap to grow your wealth, then make sure your beneficiary designations send it where you want it to go.

Sources

- 1.IRS Retirement Plan Beneficiary Rules(irs.gov)

- 2.SECURE Act and Inherited IRA Rules | Fidelity(fidelity.com)

- 3.What Is Step-Up in Basis | Fidelity(fidelity.com)

- 4.HSA Beneficiary Rules | SmartAsset(smartasset.com)

- 5.New York Estate Tax and the Cliff | NY.Gov(tax.ny.gov)

- 6.Transfer on Death Accounts | FINRA(finra.org)

- 7.2026 Federal Estate Tax Exemption | Morgan Lewis(morganlewis.com)

- 8.Life Insurance and Probate | FINRA(finra.org)