Wealth & Will

What Happens to Your 401(k) When You Die? Probate, Beneficiaries, and Heir Taxes

No probate for named beneficiaries. Learn what happens to your 401(k) at death, the 10-year rule, spouse rollover options, and how to avoid tax surprises for your heirs.

Your 401(k) does not go through probate if you have named a beneficiary—it passes directly to them, outside your will. If you haven’t named one, your plan’s default rules decide who receives it: many 401(k) plans (and ERISA’s spousal rules) pay a surviving spouse first, with children or your estate as fallbacks—and only the estate route runs through probate. If you named your estate, it goes through probate. Your beneficiary designation is separate from your will and overrides it.

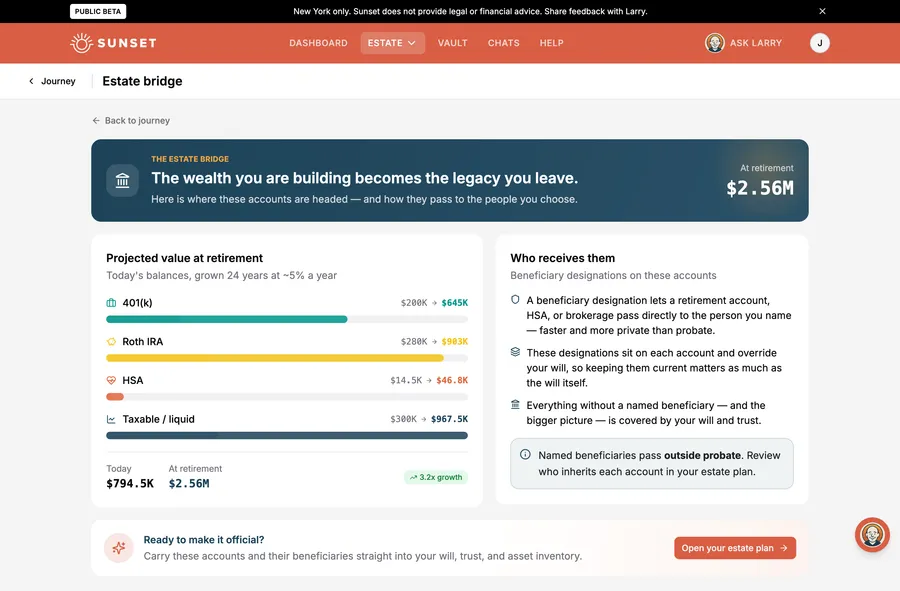

This is one of the most important estate-planning levers you control. A 401(k) with a named beneficiary is a non-probate asset, meaning it avoids the lengthy, costly legal process that applies to assets named in your will. That speed and simplicity is why coordinating your beneficiary designations with your overall estate plan is so crucial.

Why a named beneficiary beats your will

When you name a beneficiary on your 401(k), the plan administrator pays them directly after you die. No court involvement. No delays. No probate fees.

Compare this to assets that do go through probate—your house, your car, your bank accounts without transfer-on-death forms. Those assets are listed in your will, but your will has to be filed with the probate court, validated, and executed by a judge. In New York, probate can take six months to over a year and can cost several thousand dollars in legal and court fees.

Your 401(k) skips all of that. The moment your beneficiary provides a death certificate to the plan, the money is on its way to them.

But there is a catch: if you name no one, your plan’s default rules decide. Many 401(k) plans (and ERISA’s spousal protections) pay a surviving spouse first, then children—often without probate. It’s when the plan’s default is your estate, or there’s no qualifying relative, that the money lands in your estate and your heirs wait months in court to access it.

Your 401(k) beneficiary form is not your will—it is stronger

Your beneficiary designation overrides your will, even if you wrote “give all my money to my sister” in your will and named your spouse on the 401(k) form. The plan administrator follows the form on file, not the will. Update it whenever your life changes: marriage, divorce, birth of children, or a significant change in who you want to provide for.

What happens to your 401(k) if you name your spouse

A spouse has a unique legal privilege that no other beneficiary has: they can treat the inherited 401(k) as their own.

The most common and tax-smart move is a spousal rollover. Your spouse can roll the entire 401(k) balance into their own IRA. Once they do this, they follow normal IRA rules—no distributions required until they reach their own RMD age (73 for those born 1951–1959, or 75 if born in 1960 or later). One important caution: once the money is in their own IRA, withdrawals before age 59½ are subject to the usual 10% early-withdrawal penalty (the normal exceptions still apply). A surviving spouse who is younger than 59½ and might need the money sooner should compare a rollover against keeping the funds in an inherited IRA instead—where death-beneficiary withdrawals avoid the 10% penalty at any age (see below).

This is powerful because it delays taxes. Instead of your spouse facing a large taxable distribution in year one (which could push them into a higher tax bracket and trigger other tax consequences), they can let the money grow tax-deferred and take withdrawals gradually when it suits them.

Another option: your spouse can treat themselves as the deceased account owner. This is called the “spousal election” under SECURE 2.0 Section 327, and it lets them use the Uniform Lifetime Table to calculate required minimum distributions if they later become subject to RMDs.

If your spouse doesn’t do a rollover and instead takes the 401(k) as an “inherited IRA,” they must take required minimum distributions (RMDs) based on their life expectancy—but they can withdraw penalty-free at any age, which can be useful for early retirees.

Coordinate your spousal 401(k) with your overall plan

If you’re married and you have a traditional 401(k), your spouse is the automatic beneficiary in most plans unless you’ve explicitly named someone else. Check your plan documents. If your spouse predeceases you or you’ve divorced, update your beneficiary form immediately.

The SECURE Act 10-year rule for adult children and other heirs

If you name an adult child, sibling, friend, or anyone other than your spouse as your 401(k) beneficiary, they face a strict rule: the SECURE Act 10-year rule. They must withdraw the entire account balance by December 31 of the tenth year after your death, or face a 25% penalty on any remaining balance.

Here’s how it works in practice. Suppose you die in 2026 and name your adult daughter as beneficiary. She has until December 31, 2035 to empty the account. She can wait until year 10 and take it all at once, or spread withdrawals across all 10 years. Either way, every dollar she withdraws is ordinary taxable income in the year she withdraws it.

If she waited and took the entire $500,000 in year 10, she might face a $500,000 taxable distribution in a single year—potentially pushing her into the 37% federal tax bracket (for 2026, that’s roughly $640,600 and above for single filers). If she instead took roughly $50,000 per year, her tax bill would be spread over 10 years at lower marginal rates, saving her thousands in taxes.

The 10-year rule is strict: there’s no option to stretch withdrawals across her lifetime, as was possible before SECURE 2.0. Once your life ends, her clock starts ticking.

There are a few exceptions. If your beneficiary is disabled, chronically ill, or not more than 10 years younger than you, they may qualify as an “eligible designated beneficiary” and can take RMDs spread over their lifetime. But for most adult children and friends, the 10-year window is the rule.

No beneficiary named? Your plan’s default rules take over

If you die without naming a beneficiary—or if you named someone who predeceased you and never updated the form—your 401(k) plan’s default rules take over. Many plans pay a surviving spouse first, then children, with your estate as the last resort (ERISA generally makes a surviving spouse the default for private-sector plans). It’s when the money lands in your estate—because that’s the plan’s default or there’s no qualifying relative—that it becomes part of probate.

Once your 401(k) is in probate, the court process begins. Your executor or administrator has to petition the court, notify creditors, pay probate fees, and distribute assets according to your will (or state law if you don’t have a will). For a 401(k) in New York, this can easily take 8 to 12 months or longer.

During probate, the 401(k) is typically frozen—your heirs can’t access it, even in an emergency. And if your estate is large enough (New York’s estate tax exemption in 2026 is $7,350,000), your heirs may also face state estate taxes before they receive their inheritance.

The New York estate tax cliff applies to probate 401(k)s

If your total New York estate is close to $7.35 million, naming your estate as the 401(k) beneficiary can be costly. Unlike federal law, New York does not allow portability between spouses, so each spouse’s $7.35 million exemption (2026) must be carefully planned. If your estate exceeds approximately 105% of the exemption (about $7.7 million), you lose your entire exemption and the full estate value is taxed. Work with an estate attorney to name individual heirs as 401(k) beneficiaries instead.

Roth 401(k)s: the tax-free inheritance option

If you have a Roth 401(k)—contributions made with after-tax dollars—your beneficiaries face the same 10-year rule or spousal rollover options. But there’s a critical difference: withdrawals from an inherited Roth 401(k) are completely tax-free to your heirs, as long as the original Roth account was open for at least five years.

This makes Roth accounts one of the most powerful wealth-transfer tools. A $500,000 Roth 401(k) passed to your child becomes $500,000 of tax-free inheritance—they pay no income tax on the withdrawal.

If you’re still working and your plan offers a Roth option, consider how much to contribute each year. Unlike traditional 401(k) contributions, Roth contributions don’t reduce your current taxes, but they create tax-free income for your heirs. For many high-income earners (or for those planning to have a large estate), it’s worth redirecting some savings to Roth to create a tax-free legacy. Learn more about Roth vs. traditional for inheritance.

How your heirs will pay taxes on distributions

Every dollar your heirs withdraw from a traditional 401(k) is taxable as ordinary income—just as if they had earned it at their job. If you had a $1 million 401(k), your heirs don’t pay tax on that $1 million immediately, but they pay tax as they withdraw it.

The year your daughter takes a $100,000 distribution, she includes that $100,000 on her tax return. If her other income that year brings her total taxable income to $150,000, she pays federal income tax at her marginal rate (roughly 22% for 2026). If she takes $200,000 in a single year, that $200,000 bump could push her into the 24% or higher bracket for that year alone.

This is why spreading distributions over multiple years is almost always smarter than taking a lump sum—it keeps each year’s income lower and avoids a one-time spike into a higher tax bracket.

Whether annual withdrawals are required during those 10 years depends on your age when you die. If you die before your required beginning date for RMDs, the 10-year rule does not force annual distributions—your beneficiary can take nothing for nine years and empty the account in year 10 (useful if they expect a low-income year, such as retirement or a sabbatical). But if you die on or after your required beginning date, your beneficiary must also take an annual RMD in years 1 through 9, on top of emptying the account by year 10. Either way, most people find it safer to take steady withdrawals across all 10 years and predictably manage their tax brackets. (More on the 10-year rule and its RMD trap.)

Coordinate your 401(k) beneficiary with your estate plan

Your 401(k) beneficiary form is one of the most powerful levers in your estate plan. It sits outside your will, overrides it, and can save your heirs months of probate and thousands of dollars in legal fees.

But it only works if you update it. Life changes—marriage, divorce, the birth of children, the death of an old friend you named years ago. Every significant life change requires you to review and often update your beneficiary designations. Many people set a reminder to review all beneficiary forms every three to five years, or any time something major happens.

Your 401(k) is also one reason to coordinate with an overall estate plan. If you have a large estate (over $7 million in New York), naming individual heirs as 401(k) beneficiaries instead of your estate can help you avoid the New York estate tax cliff. If you have young children and significant assets, naming a trust as beneficiary might give you more control over when and how they inherit. See how every asset goes to your heirs in the map.

Start with the Money Roadmap

Your 401(k) is part of your broader money picture. The Money Roadmap at Sunset helps you see every account, every beneficiary, and every dollar of your estate—and ensures your will, trusts, and beneficiary forms all point in the same direction.

Your 401(k) doesn’t disappear when you die. It becomes a powerful tool to help your heirs, or a painful bottleneck if you’ve left it on autopilot. The choice is yours to make now.

Sources

- 1.What Happens to Your 401(k) When You Die — Fidelity(fidelity.com)

- 2.Retirement Topics — Beneficiary (IRS)(irs.gov)

- 3.SECURE Act — Inherited IRA Rules — Fidelity(fidelity.com)

- 4.Inherited 401(k): What to Know if You're a 401(k) Beneficiary — Fidelity(fidelity.com)

- 5.What Happens to Your 401(k) When You Die Without a Beneficiary — SmartAsset(smartasset.com)

- 6.Inherited 401(k) Rules: What Beneficiaries Need to Know — Bankrate(bankrate.com)

- 7.New York Estate Tax 2026: Exemption and the Cliff — Brevy Care(brevy.com)

- 8.Required Minimum Distributions (RMDs) — IRS(irs.gov)