Wealth & Will

Inherited IRA and the SECURE Act 10-Year Rule: What Your Beneficiaries Will Owe

Learn the SECURE Act 10-year rule for inherited IRAs: who must empty accounts by year 10, which beneficiaries are exempt, and what your heirs will owe in taxes.

If you have an IRA sitting in your account, whoever inherits it after you die will not get a tax-free stretch over decades. Instead, they face a hard 10-year deadline: empty the account completely, or face IRS penalties and a large tax bill. The only exceptions are a few categories of beneficiary—your spouse, your minor child, or someone disabled or chronically ill—who can spread withdrawals over their own lifetime instead.

This rule comes from the SECURE Act (2019), which shut down the stretch IRA for most people. Understanding who can stretch and who cannot is one of the most important moves you can make in your estate plan, because the difference between a 10-year payout and a lifetime stretch is often hundreds of thousands of dollars in taxes.

How the 10-year rule works

Your beneficiary inherits the IRA on the day you die. The 10-year clock starts January 1 of the year after your death. By December 31 of year 10, the entire account must be withdrawn and all taxes paid. There is no grace period and no exceptions for age or financial hardship.

The word stretch used to mean a beneficiary could take just a small amount each year, based on their own life expectancy, and leave the bulk of the money growing tax-deferred for decades. That option is now gone for most people.

The tax hit is real. Suppose you leave a beneficiary a 300,000 dollar inherited IRA. Over 10 years, they withdraw 30,000 dollars per year. At a 24% federal tax bracket (2026 rates), that 30,000 dollar withdrawal costs them roughly 7,200 dollars in federal tax alone—plus state income tax in New York or wherever they live. A married couple in the 35% bracket pays even more. Learn how to use Roth conversions and other strategies in your Money Roadmap.

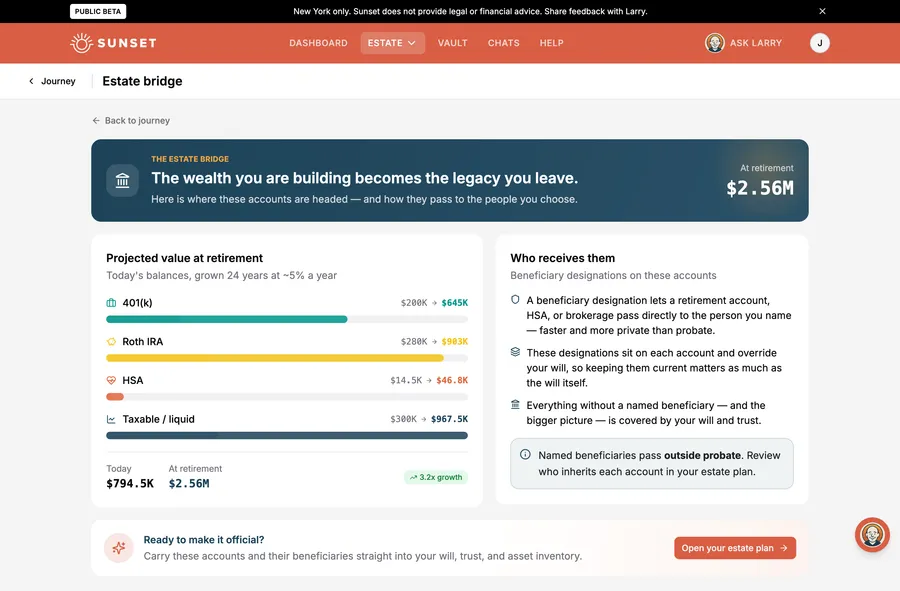

The beneficiary designation overrides your will

Your IRA beneficiary designation is separate from your will. Whoever you named as beneficiary on the IRA form—not your will—controls who inherits the money. This is true whether the beneficiary is a person, a trust, or your estate. If you haven’t updated your beneficiary form in years, it may still name an ex-spouse or someone who is no longer in your life. Check your beneficiary designations during major life changes.

Who can stretch instead: eligible designated beneficiaries

The SECURE Act created a narrow escape hatch called an Eligible Designated Beneficiary (EDB). If you name one of these people, they do not have to follow the 10-year rule. They can stretch distributions over their own life expectancy.

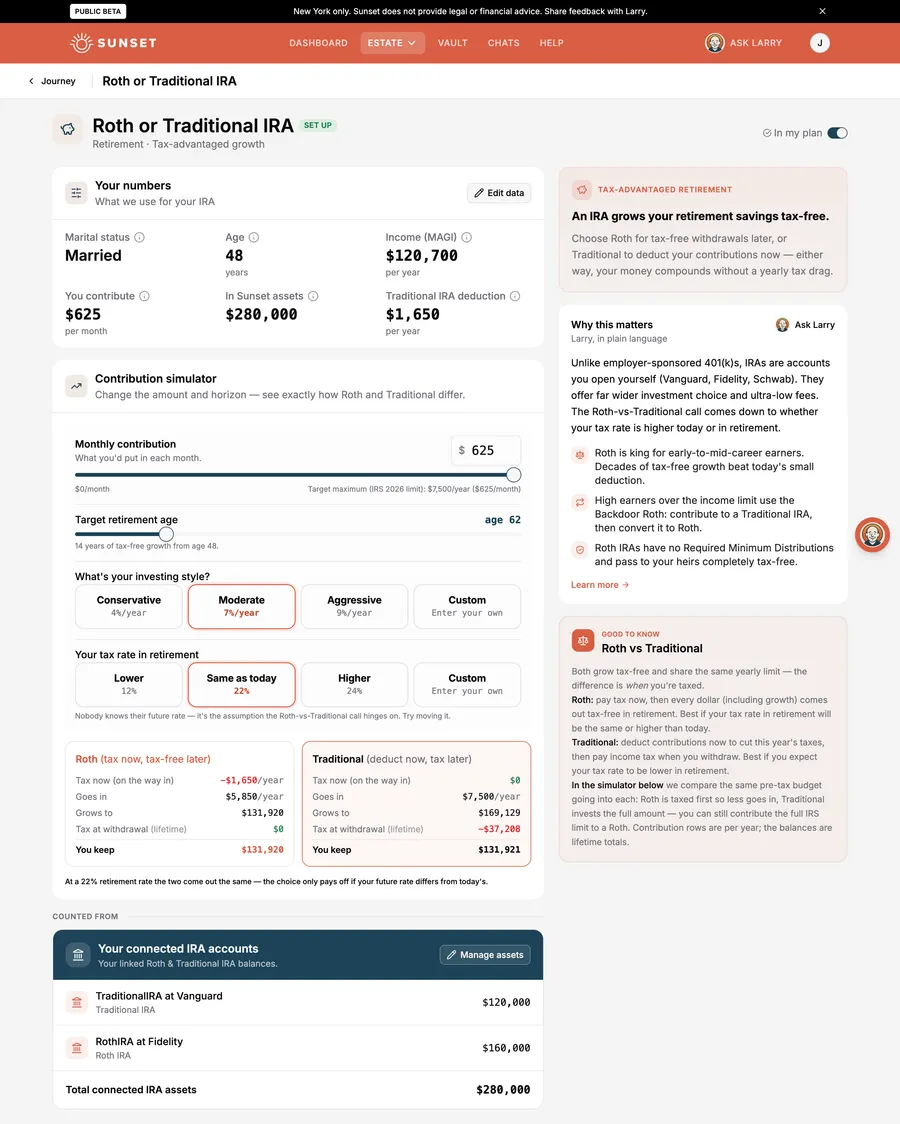

Your surviving spouse. A spouse is always an EDB and has the most flexibility. They can treat the inherited IRA as their own (no distribution deadline until their own RMD age—73, or 75 if born in 1960 or later), roll it into their own IRA, or take the stretch over their lifetime.

Your minor child. A child of yours who is under age 21 qualifies as an EDB. Once they turn 21, they flip to the regular 10-year rule. But for those young years, they can take annual distributions based on their life expectancy—a small amount until they reach adulthood.

A disabled beneficiary. If the person is blind, deaf, or unable to engage in any substantial gainful activity due to a medically determinable condition, they qualify under the Social Security definition of disability. They can stretch over their lifetime.

A chronically ill beneficiary. Someone with a serious ongoing illness who cannot perform at least two activities of daily living (bathing, dressing, toileting, transferring, continence, feeding) without substantial assistance, and has been certified by a licensed healthcare provider, qualifies. They can also stretch over their lifetime.

A beneficiary within 10 years of your age. If your beneficiary is no more than 10 years younger than you were, they qualify as an EDB and can stretch the account. This rule catches adult children in their 50s or 60s who inherit from an aging parent.

If your beneficiary does not fit one of these categories—for example, an adult child who is 15 years younger, or a grandchild, or a friend—they must follow the 10-year rule.

Naming a trust or your estate changes the payout rules—have it drafted right

How an inherited IRA pays out through a trust or an estate is one of the most technical corners of tax law, so don’t assume a single rule. A properly drafted “see-through” trust can pass the individual beneficiaries’ treatment through—an eligible designated beneficiary (like a spouse or a disabled child) may still stretch, while others fall under the 10-year rule. But a trust that isn’t see-through, or naming your estate directly, makes it a non-designated beneficiary: that generally means the 5-year rule if you die before your required beginning date, or a payout over your own remaining life expectancy if you die on or after it—not the 10-year rule at all. Name individuals when you can; if you use a trust, have an estate attorney draft it to preserve the options you want.

The RMD trap: annual withdrawals during the 10 years

Here is the detail that catches many beneficiaries off guard: if you had already started taking Required Minimum Distributions (RMD) from your IRA before you died, your beneficiary must take annual RMDs during years 1 through 9 of the 10-year period. They cannot simply wait until year 10 and withdraw the full balance.

The Required Beginning Date is April 1 of the year after you reach your RMD age—73 for those born 1951–1959, and 75 for those born in 1960 or later (SECURE 2.0 raised it from 72). If you die having already reached that date and begun RMDs, your beneficiary must take an annual RMD starting in year 1 or face the IRS penalty (25%, reduced to 10% if corrected promptly).

The calculation is simple: your remaining life expectancy, measured from the year before your death, divided into the December 31 year-end balance. IRS life expectancy tables do the math. But your beneficiary must do it right and take the money out by December 31 each year.

Roth IRA beneficiaries have a big advantage here: they do not have to take annual RMDs during the 10-year period. They can wait until year 10 to empty the account, or take money out in chunks whenever they want, as long as the entire account is gone by year 10.

| Feature | Traditional Inherited IRA | Roth Inherited IRA |

|---|---|---|

| 10-year deadline | Yes (Dec 31 of year 10) | Yes (Dec 31 of year 10) |

| Annual RMD required if original owner had begun RMD | Yes, years 1-9 | No |

| Tax on distributions | Ordinary income tax at beneficiary’s rate | Tax-free (if original account was 5+ years old) |

| Flexibility in timing | Must follow RMD schedule or wait until year 10 | Can withdraw anytime within 10 years |

| Can be stretched by spouse, disabled, minor child | Yes | Yes |

What inherited IRAs cost your beneficiaries in taxes

This is the money part. Your beneficiary will owe federal income tax, and likely state and local tax, on every dollar they withdraw from a traditional inherited IRA. Roth withdrawals are tax-free if the account has been open for 5 years or longer.

Suppose you die at age 70—before your required beginning date—with a 500,000 dollar traditional IRA and name your adult child as beneficiary. Because you died before your RBD, your child isn’t forced to take annual withdrawals, but must still empty the full 500,000 dollars by the end of year 10 (50,000 dollars per year if spread evenly). If your child is single with other income and falls into the 32% federal bracket, that 50,000 dollar annual withdrawal costs them roughly 16,000 dollars in federal tax per year, or 160,000 dollars over the 10 years. They never see that money; it goes to the IRS.

The tax bill is even larger if your child is already in the 35% or 37% bracket, or if they live in New York where the state income tax rate is up to 10.9 percent on high earners. The annual 50,000 dollar withdrawal might cost 20,000-25,000 dollars in combined federal and state tax.

If that same IRA were a Roth—and you had inherited it from your own parent years ago and already paid the taxes—your beneficiary would owe nothing. The full 500,000 dollars (or whatever it had grown to) would pass tax-free. This is why choosing a Roth IRA or converting a traditional IRA to a Roth before you die can be one of the most powerful gifts to your heirs. Compare inherited Roth vs. traditional treatment in more detail.

Coordinate your IRA with your overall estate plan

Your IRA is one piece of the picture. Some heirs benefit more from cash (like a taxable brokerage account) or appreciated investments (which get a step-up in basis); others do better inheriting a Roth IRA or 401(k) to spread out the tax pain. Sunset’s Money Roadmap helps you see which account should go to whom. Map all your assets and beneficiaries now.

Spousal options: different rules for a surviving spouse

If your spouse inherits your IRA, they have choices that no other beneficiary has.

They can treat the inherited IRA as their own (called a spousal rollover). This wipes out the 10-year rule entirely. They become the new account owner and are not required to take distributions until they reach their own Required Beginning Date (age 73, or 75 if born in 1960 or later). If they are younger, they can let the money grow for decades—though, as their own IRA, a withdrawal before age 59½ can trigger the 10% early-withdrawal penalty.

They can also roll the IRA into their own IRA (if they already have one) and simply keep it as their IRA.

Or they can elect to remain a beneficiary and take distributions over their own life expectancy—a true stretch.

This flexibility is why many married people name a spouse as beneficiary—a spouse can adapt to their own retirement timeline instead of being locked into the 10-year window. Whether it’s right for you depends on your circumstances.

From beneficiary designation to your money roadmap

The 10-year rule is not a penalty; it is the law. But it can be planned around. One of the biggest decisions is who you name as beneficiary on each account. Naming adult children is an option—just know they will face a 10-year payout and a sizable tax bill. A spouse has the most flexibility, which is why many married people name one. A disabled or chronically ill beneficiary can qualify as an EDB and stretch distributions over their lifetime. The right fit depends on your family and goals.

Your IRA works together with your 401(k), your taxable brokerage account, your life insurance, and your real estate. Together, these assets form your estate. See exactly which asset goes to whom in your Money Roadmap, and think about what your heirs will actually owe when it comes time to settle your accounts. That is the conversation that turns a pile of money into a true legacy.

Sunset’s Money Roadmap is the only place that connects every dollar you earn today to the will and inheritance plan you leave behind. Start now by naming your beneficiaries correctly, understanding the tax they will face, and building an estate plan that reflects your real wishes.

Sources

- 1.Retirement Topics - Beneficiary (IRS)(irs.gov)

- 2.Publication 590-B: Distributions from Individual Retirement Arrangements (IRS)(irs.gov)

- 3.Inherited IRA Rules & SECURE Act 2.0 Changes (Charles Schwab)(schwab.com)

- 4.Inherited IRA: Rules and RMDs Explained (Vanguard)(investor.vanguard.com)

- 5.Non-Spouse Inherited IRA Rules (Fidelity)(fidelity.com)

- 6.Extending Inherited IRA Distributions Beyond 10 Years (Kitces)(kitces.com)